In today’s Multi-Country Financial Reporting globalized business environment, companies increasingly operate across multiple countries. While international expansion unlocks growth opportunities, it also introduces complex financial reporting challenges. Differences in accounting standards, tax regulations, currencies, and compliance timelines often lead to inconsistencies in financial data.

For businesses operating in the United States, United Kingdom, United Arab Emirates (Dubai), and Canada, maintaining consistent, accurate, and compliant financial reporting is critical for decision-making, investor confidence, and regulatory adherence.

This guide explains how multi-country businesses can maintain consistency across jurisdictions while meeting local statutory requirements.

What Is Multi-Country Financial Reporting?

Multi-country financial reporting refers to the process of preparing, consolidating, and presenting financial statements for entities operating in more than one country, while ensuring:

– Compliance with local accounting and tax laws

– Alignment with global reporting standards

– Accuracy in consolidated group financials

– Transparency for stakeholders and regulators

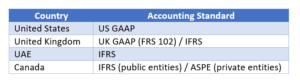

For organizations with entities in the US, UK, UAE, and Canada, this often means managing reporting under US GAAP, IFRS, UK GAAP (FRS 102), and ASPE/IFRS (Canada) simultaneously.

Key Challenges in Multi-Jurisdiction Financial Reporting

1. Different Accounting Standards

Each country follows its own accounting framework:

Reconciling these standards into one consistent group report is a major challenge.

2. Currency Conversion & FX Adjustments

Multi-country businesses deal with multiple functional currencies, leading to:

* Foreign exchange gains and losses

* Translation adjustments in consolidation

* Volatility in reported profits

Without a structured FX policy, financial statements can become misleading.

3. Local Compliance & Reporting Timelines

Each jurisdiction has different filing requirements:

US: IRS filings, state compliance, sales tax

UK: HMRC filings, Companies House submissions

UAE: VAT returns, Corporate Tax filings, ESR

Canada: CRA filings, GST/HST compliance

Misaligned deadlines often delay consolidated reporting.

4. Inconsistent Chart of Accounts

Using different account structures across countries leads to:

^ Misclassification of expenses

^ Difficulty in consolidation

^ Inaccurate management reporting

Best Practices to Maintain Consistency Across Jurisdictions

1. Standardize the Chart of Accounts (CoA)

A global chart of accounts aligned across all countries ensures:

+ Uniform expense and revenue classification

+ Faster consolidation

+ Better comparability of financial data

Local statutory accounts can still be prepared using mapping adjustments.

2. Adopt a Single Reporting Framework

While local reporting follows country-specific standards, group reporting should follow one primary framework, typically:

a. IFRS for global groups

b. US GAAP for US-parented companies

All local accounts are then converted and adjusted to the group standard.

3. Implement Centralized Accounting Policies

Documented accounting policies should cover:

– Revenue recognition

– Depreciation & amortization

– Lease accounting

– Provisions & accruals

– FX treatment

This ensures uniform application across US, UK, UAE, and Canadian entities.

4. Use Cloud-Based Accounting Systems

Cloud accounting platforms like QuickBooks, Xero, and Zoho Books enable:

– Real-time access to financial data

– Multi-currency accounting

– Centralized control with local flexibility

They are especially effective for multi-country financial reporting.

5. Establish a Robust Consolidation Process

A structured consolidation process should include:

– Intercompany reconciliation

– Elimination of intercompany transactions

– FX translation adjustments

– Uniform reporting periods

This ensures accurate group-level financial statements.

6. Align Tax & Financial Reporting

Tax rules differ significantly across jurisdictions. Regular alignment between tax computation and financial reporting avoids:

– Deferred tax errors

– Compliance risks

– Audit observations

This is particularly important for US, UK, UAE Corporate Tax, and Canadian tax filings.

Role of Outsourced Accounting in Multi-Country Reporting

Outsourcing multi-country accounting to a specialized firm provides:

* Expertise across multiple jurisdictions

* Standardized reporting processes

* Cost-effective compliance management

* Scalable finance operations

A global outsourcing partner ensures local compliance without compromising global consistency.

How FINOVATE Helps Global Businesses

FINOVATE supports businesses operating in the US, UK, UAE (Dubai), and Canada with:

~ Multi-country bookkeeping & accounting

~ IFRS, US GAAP & UK GAAP aligned reporting

~ Group consolidation & MIS reporting

~ Tax & regulatory compliance support

~ Virtual CFO & advisory services

Our structured, technology-driven approach helps businesses maintain consistent financial reporting across jurisdictions while meeting all local compliance requirements.

Frequently Asked Questions (FAQs)

How do companies manage multi-country financial reporting?

Companies manage multi-country financial reporting by standardizing accounting policies, using a unified chart of accounts, adopting a common reporting framework such as IFRS or US GAAP, and leveraging cloud-based accounting systems for consolidation.

What accounting standards apply in the US, UK, UAE, and Canada?

The US follows US GAAP, the UK follows UK GAAP (FRS 102) or IFRS, the UAE follows IFRS, and Canada follows IFRS for public entities and ASPE for private entities.

Why is consistency important in global financial reporting?

Consistency ensures accurate consolidation, reliable management reporting, regulatory compliance, and increased investor confidence across jurisdictions.

Can outsourced accounting help with multi-country compliance?

Yes, outsourced accounting firms with global expertise help businesses maintain consistent reporting while meeting local compliance and tax requirements efficiently.

Conclusion

Multi-country financial reporting is complex, but with the right framework, systems, and expertise, businesses can achieve consistency, accuracy, and compliance.

Standardized accounting policies, centralized reporting, cloud technology, and expert oversight are key to ensuring reliable financial information across the US, UK, UAE, and Canada.

For growing global businesses, consistent financial reporting is not just a compliance requirement—it’s a strategic advantage.