If you’re a first-time home buyer in Canada, the First Home Savings Account (FHSA) is one of the best tools available to help you save for your dream home.

The First Home Savings Account in Canada offers a rare combination:

a. Tax-deductible contributions and

b. Tax-free investment growth

Therefore, to take full advantage of it — and avoid costly mistakes — it’s important to understand how the First Home Savings Account in Canada works.

✅ What Is a First Home Savings Account in Canada?

The First Home Savings Account is a registered account created specifically to help Canadians save for their first home purchase.

When you contribute to this account:

– You receive a tax deduction for the amount contributed

– The money inside your account grows tax-free

– Withdrawals for qualifying home purchases are not taxed

Think of it as a hybrid between a Registered Retirement Savings Plan and a Tax-Free Savings Account, tailored for home ownership.

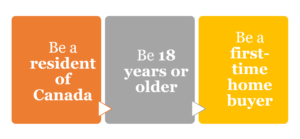

👤 Who Can Open a First Home Savings Account?

To qualify, you must:

What qualifies as a first-time home buyer?

In other words, you must not have lived in a home you or your spouse/common-law partner owned during the last four calendar years.

💰 How Much Can You Contribute?

Your contribution room begins the year you open your First Home Savings Account in Canada. Here’s what you get:

– $8,000 contribution limit in the first year

– An additional $8,000 per year going forward

– A lifetime contribution limit of $40,000

Additionally, you can carry forward unused room, but only after you open your account.

📌 Important: You may open multiple First Home Savings Accounts, but the limit applies across all accounts.

⚠️ Avoid Over-Contributing to Your FHSA

If you contribute more than your available room, you’ll be taxed 1% per month on the excess amount, until it’s withdrawn.

Example:

Suppose, you open an FHSA in 2025 and contribute $10,000.

That’s $2,000 over the limit.

As a result, you’ll owe monthly tax on the extra $2,000 at 1% per month.

Additionally, your contribution room for 2026 will be reduced to $6,000.

🛠️ How to Correct Over-Contributions

If the over-contribution came from personal income or savings:

– Fill out Form RC727

– Make a designated withdrawal to remove the excess

– Submit the form to your financial institution

Alternatively, If the over-contribution was transferred from a retirement savings plan:

– Use Form RC727 to make a designated transfer back to your retirement plan

🚫 Be careful: If you withdraw the excess without following these steps, it will be considered taxable income.

You’ll also need to file:

– Form RC728

– Schedule A (RC728-SCH-A)

You’ll use these forms to report and calculate the tax on the excess amount.

📊 Use CRA’s Estimators to Plan Wisely

The Canada Revenue Agency offers two helpful online tools to maximize your First Home Savings Account in Canada. In addition, these calculators give you a personalized projection:

– FHSA Savings Estimator

Calculates how much you could save for your home, including investment growth.

– FHSA Tax Savings Estimator

Shows how much tax you could save, based on your income and location.

Moreover, these tools already factor in the $8,000 annual limit and $40,000 lifetime limit.

📌 Frequently Asked Questions (FAQs)

To clarify further, here are some frequently asked questions:

❓ What is the First Home Savings Account in Canada?

A First Home Savings Account is a registered account that helps Canadians save for their first home. Specifically, this account offers tax-deductible contributions and Specifically, this account offers tax-deductible contributions and tax-free growth. Most importantly, withdrawals for qualifying home purchases are tax-free.

❓ How much can I contribute to a First Home Savings Account?

You can contribute $8,000 per year, up to a lifetime maximum of $40,000. Contribution room begins only once you open your first account.

❓ What happens if I over-contribute to my FHSA?

CRA taxes the excess amount at 1% per month until you remove it. To resolve an over-contribution, consider a designated withdrawal or transfer using the correct forms. These forms will also help you report and calculate the applicable tax.

❓ Is the First Home Savings Account better than a Retirement or Tax-Free Savings Account?

It depends on your goal. The FHSA is specifically designed for first-time home buyers, combining the best features of a Registered Retirement Savings Plan and a Tax-Free Savings Account. For home savings, it’s often the best choice.

🏁 Final Thoughts

A First Home Savings Account in Canada offers a powerful advantage to first-time home buyers — but only when used correctly.

Ultimately, understanding the rules, tracking your contribution room, and fixing over-contributions quickly can save you time, money, and stress.

💼 At FINOVATE, we help with tax-efficient savings strategies along with care and compliance.

👉 Need help opening or managing your First Home Savings Account?