Cryptocurrency adoption has redefined global financial systems. To begin with, Bitcoin’s launch in 2009 marking the beginning of decentralized digital transactions. Conceived by the pseudonymous Satoshi Nakamoto, Bitcoin introduced blockchain technology. This transparent and immutable distributed ledger enabling peer-to-peer transactions without intermediaries. As a result, this innovation paved the way for a rapidly growing digital asset ecosystem that challenges traditional financial institutions.

Furthermore, Cryptocurrencies function on decentralized networks, with blockchain ensuring transaction security and preventing duplication. Consequently, this disruptive financial technology has gained traction, influencing global monetary policies and regulatory frameworks.

Expanding Cryptocurrency Use and Market Influence

The rising adoption of cryptocurrencies is driven by several key factors:

• Decentralized Transactions: Eliminating intermediaries facilitates direct cross-border transfers.

• Cost Efficiency: Digital asset transactions often incur lower fees compared to conventional banking.

• Enhanced Security: Cryptographic encryption protects against fraud and cyber threats.

• Investment Potential: The volatility of crypto markets creates opportunities for substantial returns.

• Smart Contracts: Self-executing contracts reduce reliance on third-party enforcement.

• Privacy Considerations: Transactions are pseudonymous, offering a degree of confidentiality.

These advantages have driven increased cryptocurrency use in cross-border business and personal transactions.

The values of cryptocurrencies fluctuate based on supply and demand. While many experience high volatility, stablecoins—backed by tangible assets—offer price stability, making them a reliable medium for transactions. The decentralized finance (DeFi) sector further amplifies the reach of cryptocurrencies. It offers lending, borrowing, and asset trading services without traditional financial institutions. However, regulatory scrutiny is increasing due to concerns over illicit activities, fraud, and the absence of robust compliance mechanisms.

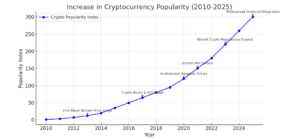

Cryptocurrency Popularity Growth

The line chart below illustrates the increasing popularity of cryptocurrencies over time. The chart highlights major milestones such as Bitcoin’s launch in 2009 and Ethereum’s introduction in 2015. It also shows the rise of institutional investment in 2020 and significant regulatory actions in the following years. The data showcases the exponential rise in crypto adoption, driven by innovation, investor interest, and financial market integration. The chart demonstrates cryptocurrency’s journey from a niche concept to a mainstream asset class.

Regulatory Developments and Compliance Measures

United States

In early 2025, the U.S. Department of Treasury and the Internal Revenue Service (IRS) introduced Form 1099-DA, requiring brokers to report digital asset transactions. While reporting cost basis remains optional for 2025, it becomes mandatory in 2026.

The IRS issued TD 10021, categorizing DeFi trading front-end providers as brokers. Additionally, they are subject to similar reporting obligations as centralized exchanges. However, developers of decentralized protocols remain outside this scope. To ease the transition, notice 2025-3 provides temporary penalty relief for brokers struggling with compliance obligations.

Cryptocurrency holdings are not currently classified as reportable under Foreign Bank and Financial Accounts (FBAR) regulations, but investors may be required to file Form 8938 if their holdings exceed the applicable threshold.

Canada

Canada has implemented a comprehensive regulatory framework to oversee digital assets, with the Canadian Securities Administrators (CSA) and Financial Transactions and Reports Analysis Centre of Canada (FINTRAC) playing key roles. Cryptocurrency exchanges must register as money services businesses (MSBs) and comply with AML and KYC requirements.

In 2023, the CSA introduced pre-registration undertakings (PRUs) for crypto trading platforms, ensuring regulatory compliance before granting operational approval. Simultaneously, the Bank of Canada is researching the feasibility of a central bank digital currency (CBDC) to align with the evolving digital economy.

India

India has taken a stringent stance on Cryptocurrency regulation, introducing a 30% tax on capital gains from crypto transactions and imposing a 1% tax deducted at source (TDS) on transfers exceeding set thresholds. While digital assets are not recognized as legal tender, the Reserve Bank of India (RBI) continues to express concerns about financial stability risks associated with the crypto sector.

In 2024, India expanded its regulatory framework by bringing crypto transactions under the Prevention of Money Laundering Act (PMLA), enforcing KYC norms, and requiring exchanges to report suspicious transactions. The government is also discussing the possibility of a licensing system for crypto service providers to enhance oversight.

United Kingdom

The Financial Conduct Authority (FCA) mandates that all crypto businesses operating in the UK obtain regulatory approval and comply with AML standards. In 2023, the UK introduced regulations requiring crypto firms to implement travel rule compliance, ensuring proper sender and receiver identification for transactions.

The UK government is also evaluating the introduction of a CBDC, informally dubbed “Britcoin,” and has prioritized stablecoin regulation to establish clear compliance standards. Additionally, UK authorities are implementing measures to combat crypto asset fraud and enhance consumer protection.

Country-Specific Regulations

• Brazil: The Cryptoassets Act designates the Central Bank of Brazil as the primary regulatory authority, mitigating fraud and enhancing compliance.

• European Union: The Markets in Crypto-Assets Regulation (MiCA) mandates licensing for service providers and requires identity verification for all transactions by 2026.

• China: A strict ban on Cryptocurrency transactions, exchanges, and mining remains in place, while the country advances its Digital Yuan (CBDC).

• Japan: The Financial Services Agency (FSA) enforces stringent AML and KYC measures, requiring crypto exchanges to share customer information.

• South Korea: The Virtual Asset Users Protection Act, enacted in 2023, enhances transparency, record-keeping, and consumer protection.

Future of Cryptocurrency: Prospects and Global Cooperation

The World Economic Forum (WEF) advocates for increased international collaboration in regulating digital assets. The organization emphasizes the importance of cross-border regulatory alignment to facilitate seamless and legally compliant digital transactions. Nations such as Singapore, Australia, the UK, Chile, and New Zealand have expressed interest in establishing new trade agreements centered on Cryptocurrency markets.

However, challenges such as interoperability, AML enforcement, and consumer protection remain critical hurdles. As Cryptocurrency adoption continues to evolve, policymakers worldwide must develop regulatory frameworks that foster innovation while ensuring financial stability and security.